For over 50 years, Ginnie Mae has worked to make affordable home financing a reality for millions of low-to-moderate income Americans, veterans, rural and tribal households, and more by ensuring that mortgage lenders can easily access funds to lend to borrowers. Ginnie Mae does this by guaranteeing the timely payment of principal and interest to investors who purchase Ginnie Mae mortgage-backed securities.

As a major source of home financing for veterans and servicemembers, the Department of Veterans Affairs (VA) offers a mortgage loan program to veterans and servicemembers and their spouses. VA home loans are originated by bank and nonbank lenders for home purchases, streamlined refinances (known as Interest Rate Reduction Refinance Loans or IRRRLs) and cash-out refinances. VA guarantees a portion of the loan amount, resulting in lower risk for the lender and more favorable terms for the borrower. Other key benefits include little to no downpayment, lower closing costs and fees, lower interest rates comparatively, and no private mortgage insurance. Borrowers pay a low one-time funding fee, except veterans with disabilities, for whom this fee is waived.

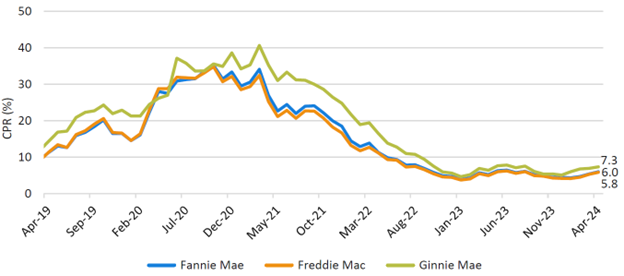

VA mortgages have historically been more likely to refinance than FHA or conventional mortgages when interest rates drop. In recent months, Ginnie Mae has observed increased refinance activity in certain cohorts, driven predominantly by VA loans. Aggregate prepayment speeds, however, remain muted and are currently below pre-pandemic levels. As of April 2024, Ginnie Mae’s fixed-rate 1 month CPR was 7.3%, compared to 6.0% and 5.8% for Fannie Mae and Freddie Mac. Current Ginnie Mae prepay speeds are significantly below the 23% CPR in Jan 2020, just before the pandemic.

Fixed Rate Aggregate 1-Month CPR

Source: Ginnie Mae Global Markets Analysis Report, May 2024

The recent increase in refinance activity comes on the heels of a decline in the 30-year mortgage rate. According to Freddie Mac’s primary mortgage market survey, rates hit a peak of 7.75% in November 2023 before falling to 6.6% percent at year end. Many loans originated at or close to peak rates last year are likely to be in-the-money for refinance in the current rate environment. As the above chart shows, prepay speeds have risen across agencies.

In the VA market, additional factors are likely contributing to increased refinance activity. VA rates for refinance loans are meaningfully lower than VA’s purchase rates (see table below.) A smaller decline in interest rates can be enough to make the refinance transaction economical for veterans. FHA and GSE refinance rates don’t exhibit a similar relationship to purchase rates, thus requiring a larger drop in rates to justify refinancing.

Weighted Average Note Rate, May 2024

| Purchase

| Non-cash out refi

| Refi rate lower than purchase by:

|

VA

| 6.32

| 5.94

| 0.38%

|

FHA

| 6.16

| 6.26

| -0.10%

|

GSEs

| 6.77

| 6.77

| 0.00%

|

Source: Bloomberg Intelligence

In addition, VA loans typically become eligible to refinance after the borrower has made six monthly payments. Thus, loans originated in late summer or fall of last year either already have, or will soon satisfy this seasoning requirement, making them refinance eligible. Lastly, VA’s IRRRL program requires no appraisal and no credit underwriting in most cases, very limited documentation, as well as the ability to include certain closing costs in the loan balance, reducing costs and lowering barriers to refinancing.

Ginnie Mae’s prepayment policies, including its seasoning requirement and monitoring of outlier prepayment speeds, were established in response to concerns about borrower harm due to refinancing activity that did not result in economic benefit to borrowers in the past. Ginnie Mae monitors prepayments monthly to identify potential outlier activity and take appropriate action. In addition, these policies provide predictability to investors and help maintain strong investor demand for our securities.

Ginnie Mae is committed to preserving access to credit by allowing eligible borrowers to refinance their mortgages to take advantage of lower rates. We are committed to our mission of maintaining a deep and liquid mortgage-backed securities (MBS) program that keeps homeownership affordable, meets the secondary market needs of our Issuers, and preserves the value of our securities.