|

|---|

|

|---|

| 3/24/2025 - APM 25-01 | | As a part of the broader effort to move all participants to a common single point of gateway entry, Ginnie Mae is announcing the migration of the pool collateral transfer and merger processes for transfers of Document Custodian responsibility. This migration of the pool collateral transfer and merger processes from GinnieNET to the Document Custodian Transfer Request application within MyGinnieMae will both streamline Issuer and Document Custodian workflows as well as provide enhanced functionality. The functionality enhancements include:

- Validation of the Pool collateral before submitting transfer/merger requests.

- User friendly “Type of Transfers Labeling” for Issuers to choose from.

- Listing of valid pools for Document Custodians to select for transfer/merger actions.

- Acknowledgment from the Issuer before transfer/merger requests are submitted.

- Enforcing Document Custodian approval response time window.

- Enhanced Issuer Profile Reporting to allow filtered reporting by Document Custodian.

The migration to MyGinnieMae will be effective April 14, 2025. Mortgage-Backed Securities Guide, 5500.3, Rev-1 (MBS Guide) Chapter 21, Appendix III-4 (Form HUD 11715) and Appendix V-01 (Document Custody Manual Chapter 7) have been updated accordingly to reflect the above noted process migration to MyGinnieMae. Detailed information and training materials will be available on the following Ginnie Mae websites:

Ginnie Mae Modernization Initiatives:

Ginnie Mae Modernization Bulletins:

If you have technical questions regarding this announcement, please contact Ginnie Mae’s centralized help desk at askGinnieMae@hud.gov. |

|

|

|---|

| 12/26/2024 - APM 24-15 | | Issuers are required to maintain a Fidelity Bond and mortgagee Errors and Omissions (E&O) insurance that meets or exceeds the minimum coverage amounts described in the Ginnie Mae Mortgage-Backed Securities Guide, Rev-1 (MBS Guide), Chapter 2, Part 7.

Effective Immediately Ginnie Mae will allow Issuers to request an extension of up to 60 days to submit their policies. Issuers must request the extension through the insurance module of Ginnie Mae Central (GMC), at least 15 days prior to the due date as specified in Appendix VI-20 of the MBS Guide.

Ginnie Mae has revised Chapter 3, Part 6, § A and Appendix VI-20 of the Ginnie Mae Mortgage-Backed Securities Guide 5500.3, Rev-1 (MBS Guide) to reflect these changes.

If you have any questions regarding the policy changes in this announcement, please contact your Account Executive in the Office of Issuer and Portfolio Management. If you have any technical questions regarding accessing GMC and/or user manuals, please email askGinnieMae@hud.gov.

|

|

|

|---|

| 12/5/2024 - APM 24-14 | | Pursuant to the Housing and Economic Recovery Act of 2008 (HERA), the Federal Housing Finance Agency (FHFA) has announced increased conforming loan limits. Accordingly, Ginnie Mae is revising its definition of High Balance Loans as follows. Effective for pools or loan packages submitted on or after January 1, 2025, a High Balance Loan is defined as a single-family forward mortgage loan with an original principal balance (minus the amount of any upfront mortgage insurance premium) that exceeds the following limits:

Maximum Loan Amounts (net of any financed MIP or Guaranty Fee

| | | | | Units

| Contiguous 48 States, District of Columbia, American Samoa, and Puerto Rico

| Alaska, Hawaii, Guam, and the U.S. Virgin Islands

| 1

| $806,500 | $1,209,750 | 2

| $1,032,650 | $1,548,975 | 3

| $1,248,150 | $1,872,225

| 4

| $1,551,250

| $2,326,875

|

High Balance Loans are eligible for Ginnie Mae MBS subject to the restrictions detailed in Ch. 9, Part 2, § B and Ch. 24 Part 2, § A(1) of the Mortgage-Backed Securities Guide 5500.3, Rev-1

(“MBS Guide”).

If you have any questions regarding this announcement, please contact your Account Executive in the Office of Issuer and Portfolio Management.

|

|

|

|---|

| 12/4/2024 - APM 24-13 | | In APM 23-03, Ginnie Mae revised pooling eligibility requirements for Re-Performing Loans allowing them to be pooled into Multiple Issuer Single Family Pools (M SF). Ginnie Mae is expanding this change to enable Re-Performing High Balance Loans to be pooled in Multiple Issuer High Balance Loan (M JM) pools.

Effective with pools submitted December 4, 2024, and thereafter, High Balance Re-Performing Loans may be securitized in M JM pools only if: (1) The borrower has made Timely Payments for the three (3) months immediately preceding the issuance month associated with the MBS, and (2) The Issue Date of the MBS is at least 120 days from the last date the loan was delinquent.

High Balance Re-Performing Loans must also meet all other applicable pooling parameters.

Re-Performing loans meeting the revised seasoning requirement announced above will be eligible for delivery through Ginnie Mae’s electronic pooling application as collateral for the C RG, M SF, and M JM pool types. Additionally, when submitting an M JM loan package that contains Re-Performing Loans in Ginnie Mae’s electronic pooling application, Issuers will be required to complete the Re-Performing Loan attestation that is currently executed for C RG and M SF submissions.

Re-Performing Loans still may not be substituted for defective loans.

Chapter 18, Part 3 §B(6) and Appendix IV-20 of the Mortgage-Backed Securities Guide 5500.3, Rev-1 (MBS Guide) have been amended in accordance with this memorandum. If you have any questions regarding this announcement, please contact your Account Executive in the Office of Issuer and Portfolio Management.

|

|

|

|---|

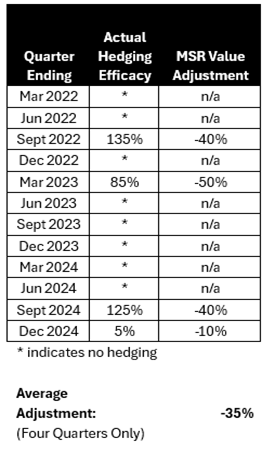

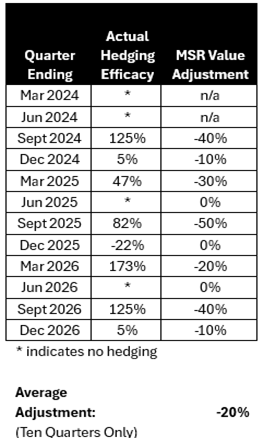

| 11/7/2024 - APM 24-12 | | To assess Issuer financial condition, Ginnie Mae requires Issuers to submit financial statements and reporting forms at regular intervals as prescribed in Chapter 3 Part 7 of the Ginnie Mae Mortgage-Backed Securities Guide, Rev-1 (MBS Guide). Among the financial requirements prescribed in Chapter 3 Part 8, Issuers are subject to Ginnie Mae Net Worth, Liquidity and Institution-wide Capital requirements. As announced in APMs 22-09 and 22-11, beginning December 31, 2024 certain Issuers and Applicants will also be required to maintain a Risk Based Capital Ratio (RBCR) of 6% which is a function of risk weighted assets to Adjusted Net Worth. Mortgage Servicing Rights (MSRs) are generally a significant portion of the Issuer’s assets and their values fluctuate due to changes in interest rates, among other market factors. By hedging MSRs, Issuers can reduce their interest rate risk exposure, and thus reduce fluctuation in MSR values. Therefore, Ginnie Mae will offer Risk Based Capital requirement relief to Issuers that demonstrate successful hedging over time.

Ginnie Mae will calculate Issuer Hedging Efficacy ratios by leveraging data submitted quarterly on the Issuer’s Mortgage Banking Financial Reporting Form (MBFRF). For the purposes of this determination, Hedging Efficacy is defined as the proportion of derivative gains/losses used to hedge MSRs relative to the change in MSR values due to market and model changes, as defined in the MBFRF. Hedging Efficacy will be used to determine the MSR Value Adjustments on a quarterly basis as shown in the table below. Ginnie Mae will then take the average of the MSR Value Adjustments over twelve quarters to determine the percentage by which the Issuer’s MSR Values will be reduced for the purpose of calculating the RBCR. The MSR Value Adjustment will not affect the Issuer’s Adjusted Net Worth (ANW), which will not be adjusted. Issuers who hedge and would like relief must Submit their MSR Value Adjustment and the resulting RBCR with their Annual Audited Financial Statements.1

If Issuers have not hedged in each of the most recent twelve (12) quarters, Ginnie Mae will use the average of hedging performance where hedging results are available, subject to the following minimum eligibility requirements: - Issuers must have hedged their MSRs in at least four (4) of the most recent twelve quarters and

- Issuers must have hedged their MSRs in at least one (1) of the most recent four (4) quarters

Additional considerations

For quarters prior to and including the quarter ending December 31, 2024, quarters in which Issuers did not hedge will not be included in determining the average hedging performance. All quarters ending in calendar year 2025 and afterward will be included in the average, regardless of whether or not the issuer hedged in a particular quarter.

Ginnie Mae will consider MSR Hedging results from Issuers who have historically hedged at affiliated entities through the quarter ending June 30, 2025. However, beginning with the quarter ending September 30, 2025, only hedging reflected on the financials of the approved Issuer entity will be considered for relief.

For Issuers approved to participate in Ginnie Mae’s program on or after December 31, 2024, Ginnie Mae, in its sole discretion, may consider hedging results for periods prior to Issuer approval that meet the minimum requirements above.

The following are two sample calculations for rolling twelve quarter periods. Example 1 demonstrates a calculation for all quarters through 2024. Example 2 represents a calculation incorporating quarters beyond 2024.

The following example illustrates the methodology required for computing the hedging adjusted RBCR. This example is based on the example provided in Chapter 3 Part 8 § A(3)(c), Institution Wide Capital, with the exception that the MSR value adjustment for hedging is applied to the MSR value.

Asset Type

| Asset Amount

| Risk Weight

| Risk Weighted Assets

| Cash and Cash Equivalents

| 100

| 0%

| 0

| Government Loans HFS

| 1,000

| 20%

| 200

| Conforming Loans HFS

| 1,500

| 20%

| 300

| Other Loans HFS

| 100

| 50%

| 50

| Gross MSRs with 35% Adjustment

| 800 x (1 - .35)=520

| 250%

| 1300*

| Other Assets

| 500

| 100%

| 500

| Total:

| 4,000

|

| 2,350

|

Total Equity (ANW)

| 600

|

|

| Excess MSRs

| 0

| | | Risk Based Capital Ratio =

| ANW-Excess MSRs

| =

| 600

|

| Risk Weighted Assets

|

| 2350

|

| | =

| 25.5%

|

* Risk weight of 250% applied to the lesser of MSRs (adjusted for hedging) or ANW

MSR hedging eligibility requirements for capital relief have been added to the MBS Guide in Chapter 3 Part 8 §A(3)(c).

If you have any additional questions about the content of this Memorandum, please contact your Account Executive in the Office of Issuer Portfolio Management directly.

_______________________________________ 1Ginnie Mae has updated the supplemental Information exhibits for the revised for the revised financial requirements Announced in APMs 22-09 and 22-11. They will be published in an upcoming APM.

|

|

|

|---|

| 9/6/2024 - APM 24-11 | | Periodically, Ginnie Mae implements minor updates to the Mortgage-Backed Securities Guide 5500.3, Rev-1 (“MBS Guide”) to ensure that its policies are clearly and accurately reflected and to notify Issuers about upcoming operational changes. Please note the following content updates being made to the MBS Guide. All updates are effective immediately.

Guide Chapters

| Guide Changes

| Page Number(s)

| Ch. 3, Part 8

| Removed references to fiscal year 2020 from the introductory section of Part 8, because the rule described in it is already in effect per APM 19-06.

| 3-7

| Ch. 3, Part 8, Section A(2)(a)

| The second part of (a)(ii) became (a)(iii) and the previous a(iii) and became a(iv) to reflect the fact that there are 4 components to the calculation referenced in this text.

| 3-9

| Ch. 7, Part 2, Section B

| Specified the exact location on Ginnie Mae's website of the checklist of documents an applicant is required to submit.

| 7-1

| Ch. 7, Part 4, Section A(4)

| Updated the link to the HUD/OIG Consolidated Audit Guide.

| 7-4

| Ch. 9, Part 2, Section B

| Added clarification to the text in parenthesis that is part of the sentence on page 9-1 which defines what a High Balance Loan is. The text now reads: "(minus the amount of any upfront mortgage insurance premium or the VA funding fee)."

| 9-1

| Ch. 11, Part 1

| Added a reference to the Digital Collateral Guide.

| 11-1

| Ch. 16, Part 8, Section B

| Replaced in subsection b(ii) the reference to Kroll with the agency's full name and the name of its score.

| 16-6

| Ch. 24, Part 2, Section A(1)(c), (3)(d)(e)

| Corrected the numbering.

| 24-1, 24-5, 24-6, 24-7, 24-8, 24-9

| Ch. 24, Part 2, Section A(1)(e)

| Given that the Targeted Lending Initiative program has been retired, GNMA removed the sentences: "For pools meeting Ginnie Mae's Targeted Lending Initiative, the minimum servicing fees will be 20, 21, and 22 basis points with a guaranty fee of 5, 4, and 3 basis points, respectively. The maximum weighted average servicing fee at issuance cannot exceed 72 basis points."

| 24-2, 24-3

| Ch. 24, Part 2, Section A(1)(e)

| The changes discussed in the first sentence of the next to last paragraph in the section were implemented some time ago, GNMA updated the language to read: 'Pursuant to Ginnie Mae II program requirements...:

| 24-2

| Ch. 26, Part 2, Section A

| Updated the links to the CME Term SOFR index and updated the name of the entity that produces it.

| 25-10, 26-11

| Ch. 33. Part 3, Section A

| Included the full name of the MBS Guide Summary of Addresses so it is consistent with the rest of the MBS Guide.

| 33-2

| App. VI-22

| Removed all references to Payment Default Status (PDS) Guide/Reporting Manual because it was not created.

| 2

|

Additional miscellaneous edits have been made to correct the formatting in Chapter 3 that are not itemized above.

If you have any additional questions about the content of this Memorandum, please contact your Account Executive in the Office of Issuer and Portfolio Management directly.

|

|

|

|---|

| 7/31/2024 - APM 24-10 | | Ginnie Mae remains dedicated to the security and integrity of all operational systems and critical technology infrastructure related to the issuance and servicing of Ginnie Mae Mortgage-Backed Securities (MBS). In support of these objectives, Ginnie Mae will be implementing Cybersecurity Incident reporting requirements. Effective immediately, Document Custodians will be required to notify Ginnie Mae of a Significant Cybersecurity Incident, as described below.

A Significant Cybersecurity Incident (Cyber Incident), is an event that actually or potentially jeopardizes, without lawful authority, the confidentiality, integrity, or availability of information or an information system; or constitutes a violation or imminent threat of violation of security policies, security procedures, or acceptable use policies and has the potential to directly or indirectly impact the Document Custodian’s ability to meet its obligations as required by Appendix V-01—Document Custodian Manual in the Mortgage-Backed Securities Guide (MBS Guide). The requirement to notify Ginnie Mae applies to all Document Custodians.

Document Custodians must notify Ginnie Mae within 48 hours of detection that a Cyber Incident may have occurred. The notification must be sent to Ginnie Mae via email to: Ginnie_Mae_Cybersecurity_Incident@hud.gov and contain the following information: - Date/time of Cyber Incident,

- A summary of the incident based on what is known at the time of notification,

- Designated point(s) of contact who will be responsible for coordinating any follow-up activities on behalf of the notifying party.

Once the notification is received, representatives from Ginnie Mae will contact the designated point of contact to obtain additional information and establish the appropriate level of engagement needed depending on the scope and nature of the incident. Ginnie Mae is reviewing its information security requirements with the intent of further refining its information security, business continuity and reporting requirements.

If you have any questions about the policy announced in this APM, please contact your Account Executive directly.

|

|

|

|---|

| 5/31/2024 - APM 24-09 | | On May 31, 2024, Ginnie Mae will publish an updated Digital Collateral Program Guide (eGuide). This new eGuide contains several changes and clarifications to Digital Collateral Program policy and procedures, including:

- Section 2140.00 – Clarified that Issuers originating eNotes as well as those aggregating eNotes are eligible to participate in the Digital Collateral Program.

- Section 2300.00 – Clarified that eIssuers and eCustodians are expected to maintain their dedicated personnel contacts with Ginnie Mae throughout their participation in the Digital Collateral Program.

- Sections 2420.00 and 2620.00 – Updated requirements for Qualified eClosing Systems and Qualified eVaults to align with new/updated industry standards and requirements.

- Section 2430.00 – Added requirement that eIssuers retain the eClosing audit trail for any eMortgage delivered in a digital pool or loan package.

- Sections 2440.00, 2550.00, and 2680.00 – New requirements that eIssuers and eCustodians notify Ginnie Mae when they change eClosing System, eNote, or eVault providers.

- Section 2630.00 – Clarified potential scope of required practices transactions applicable to eIssuer and eCustodian applicants.

- Section 2660.00 – Updated annual audit requirement for eVaults.

- Section 3400.00 – Expansion of the permitted digital collateral pool types to include C ET pools for extended term loans, which often result from a loan modification.

- Section 3500.00 – Updated to permit commingling of eMortgages with mortgage loans having a paper promissory note in the same Ginnie Mae pool or loan package.

- Section 4300.00 – Updated to reflect the transition from GinnieNET to the Ginnie Mae Single Family Pool Delivery Module (SFPDM).

- Section 5330.03 – Clarified that eCustodians are expected to confirm eNotes contain the required eNote heading and clauses during Initial Certification and that during Initial Certification the MERS® eRegistry field for Controller Delegatee for Transfers may either be blank or name the eCustodian.

- Section 5820.00 – Clarified requirements for handling of eNote defects.

- Section 6200.00 – Clarified requirements for removal of Ginnie Mae from the Secured Party field on the MERS® eRegistry.

- Section 6250.00 – Removed required notification to Ginnie Mae prior to assumption involving an eMortgage and clarified that the assumption must be reported to the MERS® eRegistry.

- Section 6260.00 – Clarified expectations regarding handling of New York Consolidation Extension and Modification Agreements (NY CEMAs).

- Section 6300.00 – Clarified restrictions on subservicing Digital Pool/Loan Packages.

- Section 6430.00 – Clarified requirements and best practices for Transfers of Issuer Responsibility applicable Digital Pool/Loan Packages.

- Section 6600.00 – Clarified that all Digital Pool/Loan Packages (whether consisting entirely of eMortgages or of eMortgages commingled with mortgage loans having a paper promissory note) are ineligible for Ginnie Mae’s Pools Issued for Immediate Transfer (PIIT) program.

- Glossary – Revised term “Digital Pool or Loan Package” to “Digital Pool/Loan Package” and redefined to include both Ginnie Mae pools and loan packages consisting entirely of eMortgages as well as pools and loan packages in which eMortgages are commingled with mortgage loans having a paper promissory note.

If you have any additional questions about the content of this Memorandum, please contact your Account Executive in the Office of Issuer and Portfolio Management directly.

|

|

|

|---|

| 5/20/2024 - APM 24-08 | | Ginnie Mae is introducing recovery planning requirements for Issuers that are not subject to federal regulation by the agencies listed in Chapter 03, Part 8 §A(3)(a) whose portfolios equal or exceed a remaining principal balance (“RPB”) of $50,000,000,000 ($50 billion) at the end of the calendar year. Covered Issuers with the requisite portfolio size as of December 31, 2024 will be required to prepare and submit recovery plans to Ginnie Mae no later than June 30th, 2025 via email to GNMARecPln@hud.gov. Ginnie Mae is making this change as part of its holistic approach to program governance to assure rapid and orderly servicing transfer in the case of an Issuer’s material distress or failure. These plans must contain all relevant material, as described in MBS Guide Appendix VI-23 of the Ginnie Mae Mortgage-Backed Securities Guide 5500.3, Rev-1 (MBS Guide), including but not limited to the elements described below:

- Corporate structure—Organizational charts; location; key personnel; contact information for the Issuer, any parent or subsidiary; mapping of critical operations and core business lines. Identification of interdependencies within the company and with material entities; counterparties that could have a material impact on business operations; and those to whom the Issuer has pledged MBS collateral and where that collateral is held.

- Information systems--Detailed inventory and mapping of key management information systems and applications; and the process by which supervisory or regulatory agencies could access those systems and applications.

- Recovery planning—Plan to meet the requirements of the Ginnie Mae Guaranty Agreement; Plan to unwind its Ginnie Mae MBS portfolio in a timely and efficient manner; and business continuity plans.

Covered Issuers must demonstrate that they have assessed the challenges that their organizational structure and business activities pose, and that they have taken actions to address and mitigate the related risks. Ginnie Mae will not issue any penalties or punitive actions related to information submitted in the recovery plans. All information provided in the recovery plans will be treated by Ginnie Mae as confidential and will not be publicly released.

Every two years, covered Issuers will be required to update and resubmit their recovery plans or attest that the most recently approved recovery plan remains current. These submissions are due no later than June 30th of the following calendar year. Notwithstanding this requirement, if the covered Issuer makes a material change to its recovery plan between required submissions, covered Issuers must report the change to Ginnie Mae by submitting an updated version of the entire recovery plan, with all changes highlighted, no later than 60 days after making the material change. See MBS Guide Chapter 3 Part 18, § D and Appendix VI-23 for more details.

If you have questions, please contact your Account Executive in the Office of Issuer and Portfolio Management directly.

|

|

|

|---|

| 5/20/2024 - APM 24-07 | | In July of 2020, Ginnie Mae implemented its Digital Collateral Program Pilot to support the Department of Housing and Urban Development’s (HUD) Strategic Plan with respect to modernization and digitization of Ginnie Mae’s Mortgage-Backed Securities (MBS) program, as well as to respond to industry requests to optimize Issuer digital environments and align with current industry practices. During this time, Ginnie Mae refined processes to monitor growth in the new program and opened the program to allow any Issuer to apply to participate in June of 2022. To promote liquidity and increase participation in the Digital Collateral Program, Ginnie Mae will permit the securitization of Digital Collateral into the same pools as its traditional paper collateral (commingling) effective with June 1, 2024 issuances.

Only Issuers who are separately approved for participation in the Digital Collateral Program (eIssuers) are eligible to deliver Digital Collateral into Ginnie Mae MBS. eIssuers who wish to commingle must continue to abide by all established pooling parameters for all pooled loans, which includes additional existing parameters for eNotes within the commingled pool. In addition, as announced in Modernization Bulletin No. 34 in December 2023, all eIssuers must utilize the eNote indicator within Ginnie Mae’s pooling issuance system SFPDM to indicate whether or not a pooled loan is an eNote. Additionally, eIssuers must utilize an approved eCustodian for any pools that contain Digital Collateral.

Digital Collateral, which consists of mortgage loans where the promissory notes are Eligible eNotes, will continue to be eligible for the same pool types for which they are currently eligible, as published in Ginnie Mae’s Digital Collateral Guide, (eGuide) which is Appendix V-07 of the Ginnie Mae Mortgage-Backed Securities Guide 5500.3, Rev-1 (MBS Guide). An updated eGuide reflecting this change will be published prior to June 1, 2024 and will provide further updates.

If you have any additional questions about the content of this Memorandum, please contact your Account Executive in the Office of Issuer and Portfolio Management directly.

|

|