Focused on affordability for more than 50 years

Ginnie Mae makes affordable housing finance possible for America's homeowners and renters.

Learn Morehttps://www.ginniemae.gov/Carousel%20Area%20Images/Rotating%20Images/Hero-01.png

https://www.ginniemae.gov/Carousel%20Area%20Images/Rotating%20Images/Hero-02.png

Message

Message field can not exceed 510 characters

Message field can not exceed 510 characters

Please verify that you are not a robot

URL

https://www.ginniemae.gov/newsroom/HAPS/Pages/Post.aspx?PostID=31

Message sent!

|

|---|

|

Ginnie Mae’s current position in fixed-income markets is vastly different than it was a decade ago. Our outstanding mortgage-backed securities (MBS) have grown steadily over the past ten years as the agency has fulfilled its mission to support the government-guaranteed mortgage market by attracting broad investor support for the government-guaranteed MBS product. Consider the numbers: Over the past decade, the value of Ginnie Mae’s outstanding MBS more than doubled from $888 billion at the end of fiscal year 2009 to $2.1 trillion at the end of fiscal year 2019.

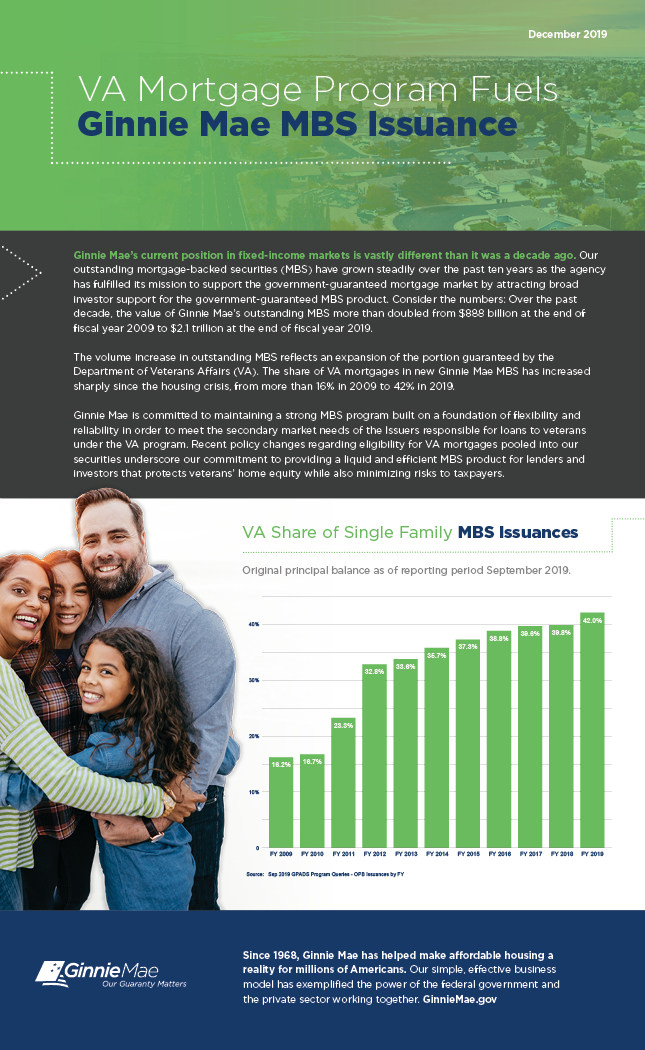

The volume increase in outstanding MBS reflects an expansion of the portion guaranteed by the Department of Veterans Affairs (VA). The share of VA mortgages in new Ginnie Mae MBS has increased sharply since the housing crisis, from more than 16% in 2009 to 42% in 2019.

Ginnie Mae is committed to maintaining a strong MBS program built on a foundation of flexibility and reliability in order to meet the secondary market needs of the Issuers responsible for loans to veterans under the VA program. Recent policy changes regarding eligibility for VA mortgages pooled into our securities underscore our commitment to providing a liquid and efficient MBS product for lenders and investors that protects veterans’ home equity while also minimizing risks to taxpayers.

|

Meet the Executive

|

|

Stay connected on what's happening in the government housing finance sector

Already a subscriber? Login to update your preferences

here

.