To assess Issuer financial condition, Ginnie Mae requires Issuers to submit financial statements and reporting forms at regular intervals as prescribed in Chapter 3 Part 7 of the Ginnie Mae Mortgage-Backed Securities Guide, Rev-1 (MBS Guide). Among the financial requirements prescribed in Chapter 3 Part 8, Issuers are subject to Ginnie Mae Net Worth, Liquidity and Institution-wide Capital requirements. As announced in APMs 22-09 and 22-11, beginning December 31, 2024 certain Issuers and Applicants will also be required to maintain a Risk Based Capital Ratio (RBCR) of 6% which is a function of risk weighted assets to Adjusted Net Worth. Mortgage Servicing Rights (MSRs) are generally a significant portion of the Issuer’s assets and their values fluctuate due to changes in interest rates, among other market factors. By hedging MSRs, Issuers can reduce their interest rate risk exposure, and thus reduce fluctuation in MSR values. Therefore, Ginnie Mae will offer Risk Based Capital requirement relief to Issuers that demonstrate successful hedging over time.

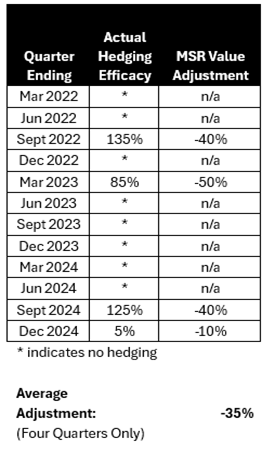

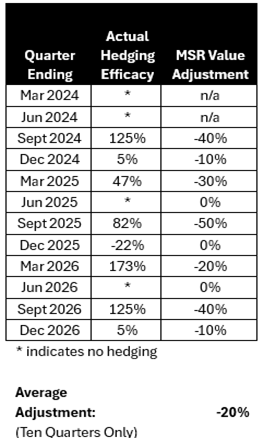

Ginnie Mae will calculate Issuer Hedging Efficacy ratios by leveraging data submitted quarterly on the Issuer’s Mortgage Banking Financial Reporting Form (MBFRF). For the purposes of this determination, Hedging Efficacy is defined as the proportion of derivative gains/losses used to hedge MSRs relative to the change in MSR values due to market and model changes, as defined in the MBFRF. Hedging Efficacy will be used to determine the MSR Value Adjustments on a quarterly basis as shown in the table below. Ginnie Mae will then take the average of the MSR Value Adjustments over twelve quarters to determine the percentage by which the Issuer’s MSR Values will be reduced for the purpose of calculating the RBCR. The MSR Value Adjustment will not affect the Issuer’s Adjusted Net Worth (ANW), which will not be adjusted. Issuers who hedge and would like relief must Submit their MSR Value Adjustment and the resulting RBCR with their Annual Audited Financial Statements.1

If Issuers have not hedged in each of the most recent twelve (12) quarters, Ginnie Mae will use the average of hedging performance where hedging results are available, subject to the following minimum eligibility requirements:

- Issuers must have hedged their MSRs in at least four (4) of the most recent twelve quarters and

- Issuers must have hedged their MSRs in at least one (1) of the most recent four (4) quarters

Additional considerations

For quarters prior to and including the quarter ending December 31, 2024, quarters in which Issuers did not hedge will not be included in determining the average hedging performance. All quarters ending in calendar year 2025 and afterward will be included in the average, regardless of whether or not the issuer hedged in a particular quarter.

Ginnie Mae will consider MSR Hedging results from Issuers who have historically hedged at affiliated entities through the quarter ending June 30, 2025. However, beginning with the quarter ending September 30, 2025, only hedging reflected on the financials of the approved Issuer entity will be considered for relief.

For Issuers approved to participate in Ginnie Mae’s program on or after December 31, 2024, Ginnie Mae, in its sole discretion, may consider hedging results for periods prior to Issuer approval that meet the minimum requirements above.

The following are two sample calculations for rolling twelve quarter periods. Example 1 demonstrates a calculation for all quarters through 2024. Example 2 represents a calculation incorporating quarters beyond 2024.

The following example illustrates the methodology required for computing the hedging adjusted RBCR. This example is based on the example provided in Chapter 3 Part 8 § A(3)(c), Institution Wide Capital, with the exception that the MSR value adjustment for hedging is applied to the MSR value.

Asset Type

| Asset Amount

| Risk Weight

| Risk Weighted Assets

|

Cash and Cash Equivalents

| 100

| 0%

| 0

|

Government Loans HFS

| 1,000

| 20%

| 200

|

Conforming Loans HFS

| 1,500

| 20%

| 300

|

Other Loans HFS

| 100

| 50%

| 50

|

Gross MSRs with 35% Adjustment

| 800 x (1 - .35)=520

| 250%

| 1300*

|

Other Assets

| 500

| 100%

| 500

|

Total:

| 4,000

|

| 2,350

|

Total Equity (ANW)

| 600

|

|

|

Excess MSRs

| 0

| | |

Risk Based Capital Ratio =

| ANW-Excess MSRs

| =

| 600

|

| Risk Weighted Assets

|

| 2350

|

| | =

| 25.5%

|

* Risk weight of 250% applied to the lesser of MSRs (adjusted for hedging) or ANW

MSR hedging eligibility requirements for capital relief have been added to the MBS Guide in Chapter 3 Part 8 §A(3)(c).

If you have any additional questions about the content of this Memorandum, please contact your Account Executive in the Office of Issuer Portfolio Management directly.

_______________________________________

1Ginnie Mae has updated the supplemental Information exhibits for the revised for the revised financial requirements Announced in APMs 22-09 and 22-11. They will be published in an upcoming APM.